Foreclosure refers to a legal process in which a lender attempts recover the balance on a loan from a borrower, who has stopped making regular payments. The lender then forces the borrower sell collateral used to secure his loan. This procedure can have many ramifications, including the negative impact on a borrower’s credit.

Get current with your mortgage payments to prevent foreclosure

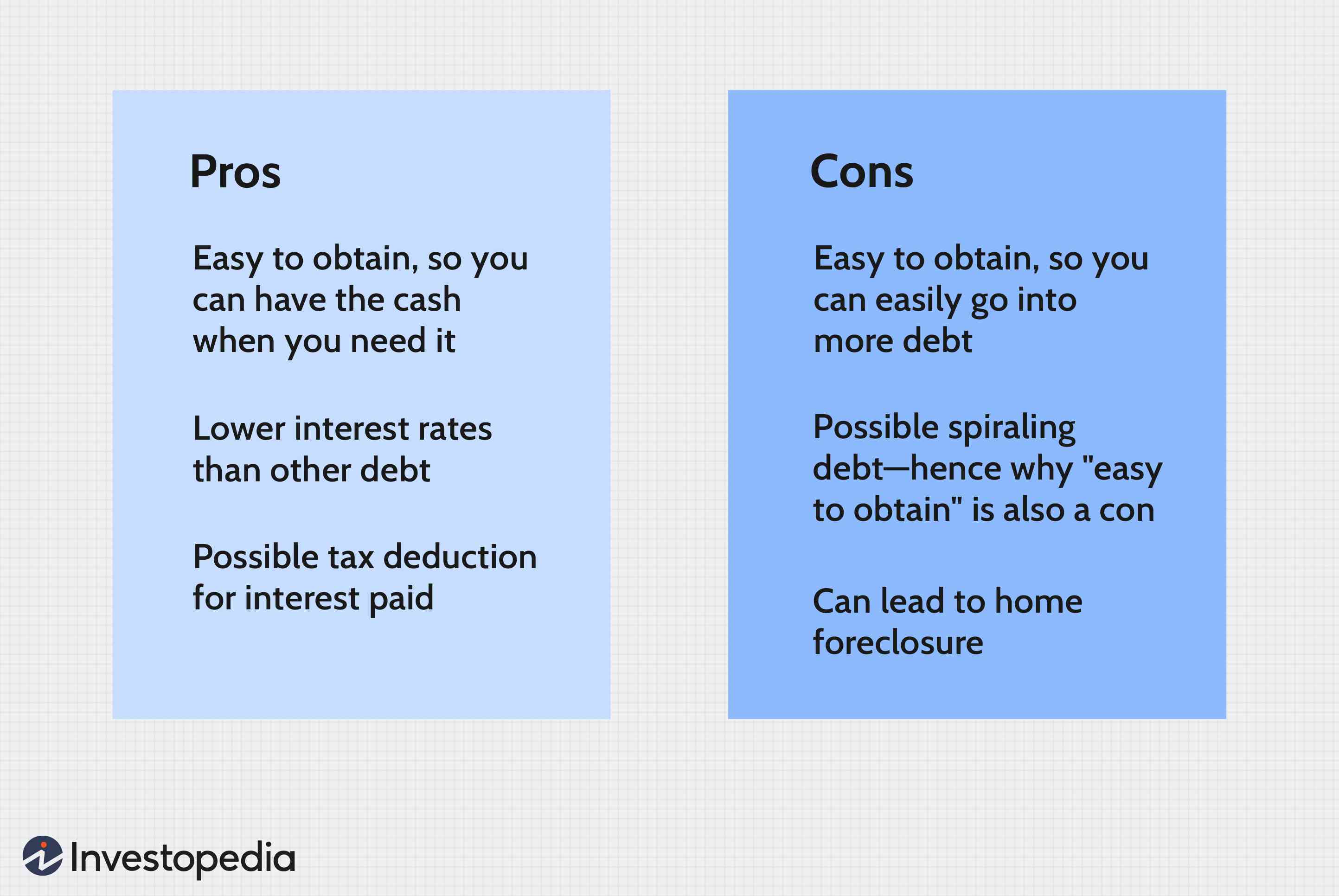

You can avoid foreclosure by paying your mortgage on time. This can be very difficult if you fall behind on your mortgage payments. There are financial aid programs that will help you catch up. These programs can even partially help you to pay your home mortgage. You might also consider a parttime job or cutting back your expenses. By paying down your debts and saving money, it is possible to avoid foreclosure and even save your house.

You can also speak with a mortgage counselor. These counselors are usually free or very low-cost and can provide valuable information on how to manage your finances. These counselors are available to help you sort through the different options you have, such as applying in a mortgage modification program.

You have options to get out of foreclosure

There are many options available for people facing foreclosure. Some of these options include loan modifications or deeds-in-lieu of foreclosure, short sales and government loans. Depending on your individual situation, one or more of these options may be right for you. These options may allow you to save your home from foreclosure.

First, contact your mortgage servicer to inform them that you no longer have the ability to pay the monthly payments. They can begin foreclosure proceedings against you if they do not receive your notification. But if they do start foreclosure proceedings against you, you should understand that your losses as well any junior loans may remain your responsibility. You could also face other consequences if you fail to pay your mortgage.

Effects of foreclosure on credit

You can experience a significant drop in your credit score if you are subject to foreclosure. The second most damaging negative event on your credit report is foreclosure, after bankruptcy. It can make borrowing money or getting credit cards more difficult. For this reason, many lenders won't even consider an applicant who has a foreclosure on their credit report. However, you can still improve your credit score.

It can take years for the credit effects of foreclosure to be reversed. It can take as long as two years to get a foreclosure removed from your credit reports. You may not be eligible for a conventional loan if you lose your home due to foreclosure or file bankruptcy within one year. The longer you wait to re-apply for a loan, the higher your interest rate will be.

Legal process of foreclosure

Foreclosures are a stressful and lengthy process. The lender might file a civil action against the homeowner to force them from the home if they are unable to pay their mortgage. Foreclosure costs can also be pursued by the lender. If the borrower resists, they might be granted an additional year to settle the debt.

It doesn't matter what the reason behind foreclosure, it is important that you know your rights. Foreclosures could negatively impact your credit. If faced with this, you should immediately seek legal counsel. There are several ways you can fight foreclosure.

FAQ

How much money do I need to purchase my home?

This can vary greatly depending on many factors like the condition of your house and how long it's been on the market. Zillow.com shows that the average home sells for $203,000 in the US. This

What are the advantages of a fixed rate mortgage?

Fixed-rate mortgages lock you in to the same interest rate for the entire term of your loan. This guarantees that your interest rate will not rise. Fixed-rate loans have lower monthly payments, because they are locked in for a specific term.

What is the cost of replacing windows?

Replacing windows costs between $1,500-$3,000 per window. The exact size, style, brand, and cost of all windows replacement will vary depending on what you choose.

How long does it take to sell my home?

It depends on many factors including the condition and number of homes similar to yours that are currently for sale, the overall demand in your local area for homes, the housing market conditions, the local housing market, and others. It can take from 7 days up to 90 days depending on these variables.

Can I get another mortgage?

Yes. However, it's best to speak with a professional before you decide whether to apply for one. A second mortgage is usually used to consolidate existing debts and to finance home improvements.

Do I need flood insurance

Flood Insurance covers flooding-related damages. Flood insurance can protect your belongings as well as your mortgage payments. Learn more information about flood insurance.

Statistics

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How do you find an apartment?

Finding an apartment is the first step when moving into a new city. This involves planning and research. It includes finding the right neighborhood, researching neighborhoods, reading reviews, and making phone calls. This can be done in many ways, but some are more straightforward than others. These are the steps to follow before you rent an apartment.

-

Researching neighborhoods involves gathering data online and offline. Online resources include Yelp and Zillow as well as Trulia and Realtor.com. Offline sources include local newspapers, real estate agents, landlords, friends, neighbors, and social media.

-

Review the area where you would like to live. Review sites like Yelp, TripAdvisor, and Amazon have detailed reviews of apartments and houses. You can also check out the local library and read articles in local newspapers.

-

To get more information on the area, call people who have lived in it. Ask them what the best and worst things about the area. Ask if they have any suggestions for great places to live.

-

Check out the rent prices for the areas that interest you. Consider renting somewhere that is less expensive if food is your main concern. If you are looking to spend a lot on entertainment, then consider moving to a more expensive area.

-

Find out more information about the apartment building you want to live in. For example, how big is it? How much does it cost? Is it pet friendly What amenities do they offer? Can you park near it or do you need to have parking? Are there any rules for tenants?