Perhaps you're in debt. There are several types of liens, including Tax liens, Real estate liens, and Judgment liens. To protect yourself, it is essential to know which type lien you have on your property. You should not only learn about the types of liens but also know your state's statute of limitations.

Real estate liens

Real estate liens are important when you're looking to buy a property. These liens can be used to secure payment for a debt. They are used to secure payment on a debt. If you don't pay the loan, the lender may foreclose. There are two main types - voluntary and involuntary.

Tax liens

Although tax liens can be a great investment, they are notoriously risky. Investors should conduct their own research before making a decision. Experts advise investors to stay away from properties that have significant environmental damage, as this can affect their ability to gain ownership if the property goes into foreclosure. They should also research liens on the property, recent tax sales, and recent sale prices of comparable properties. Be sure to look for other liens as well, as this can make ownership more complicated. Be aware that tax lien information might be outdated or inaccurate.

Judgment liens

A judgment lien is a debtor's right to collect on a debt that was awarded to them by a court. It attaches to the debtor's real estate and lasts for five years. This certificate can be obtained by filing a certified of judgment with a clerk of common pleas of the county in which the debtor resides. This real property includes land and any fixtures.

Judicial liens

For creditors, judgment liens can prove to be an extremely powerful tool when it comes down to real estate. These liens are placed onto a debtor's real estate to ensure that the debtor repays the entire amount. It is simple to put a judgment on real estate. The first step is to request an abstract from the court of entrance. This abstract is then filed with all the counties in which real estate is owned by the debtor. The judgment can be filed in all counties where the debtor owns real estate.

Bank and judgment liens

If a creditor gets a judgment against a person, they can put a lien on that person's property in order to collect the debt. This lien is recorded at the county office's land records. Liens can be imposed on properties in a number of circumstances, including to obtain payment for money judgments, back taxes, and attorney's fees.

Sheriff's sale

If you want to prevent a sheriff's sale from taking place, you need to know how the process works. First, the owner must file the "PRAECIPE", which is a form that informs the Clerk of Courts about the intention to sell the property. The PRAECIPE serves to notify the court that an owner wants to sell the property. This document must be filed at least 30 calendar days prior to the sale date.

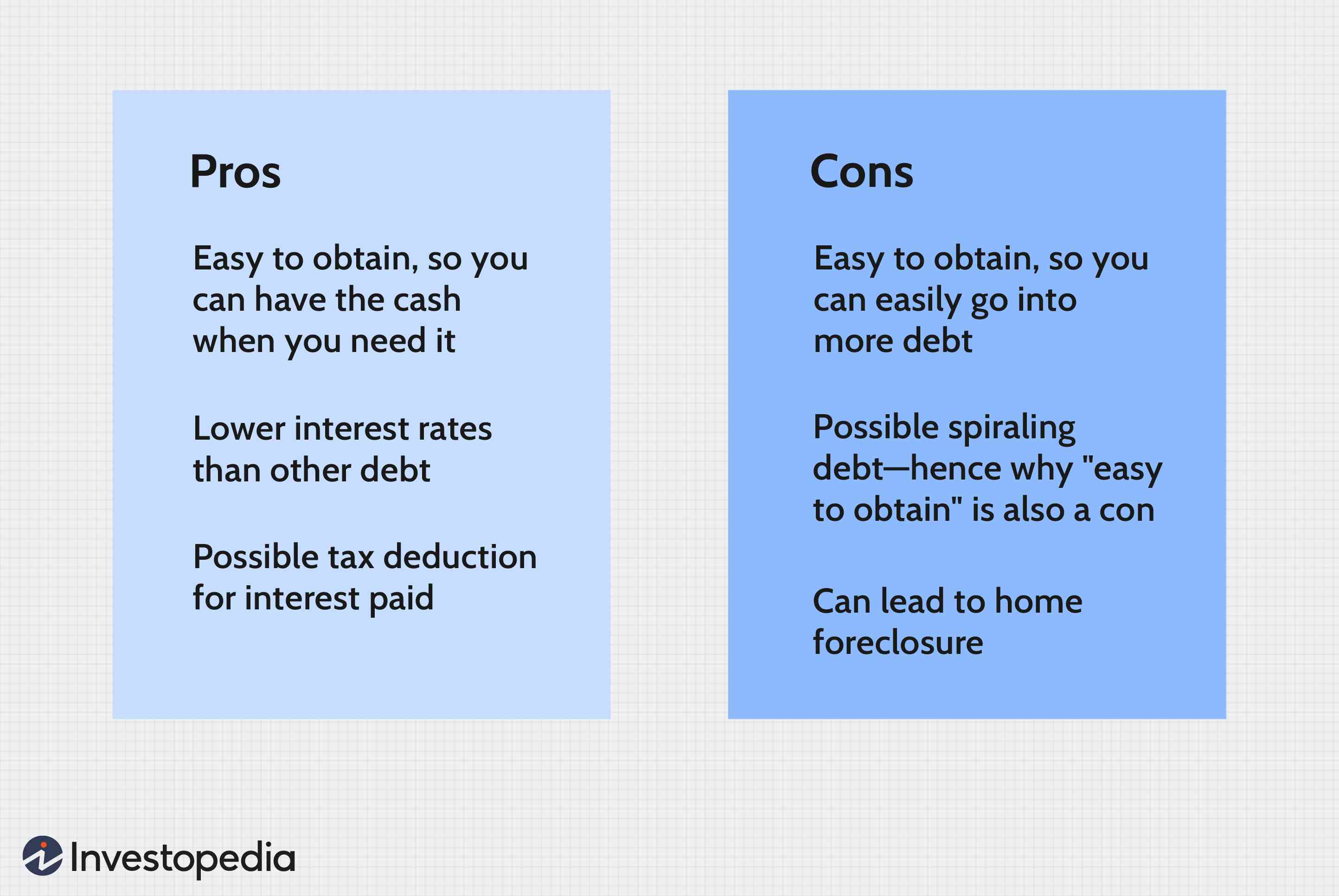

Refinance using a lien

Many people wonder if they are able to refinance with liens against their property. Liens are a common situation, but it is not impossible to get a refinancing. However, you must make sure that you have paid off the liens on your property before you can apply for a loan. It can have a negative impact on your credit rating.

FAQ

How do I calculate my rate of interest?

Market conditions can affect how interest rates change each day. The average interest rates for the last week were 4.39%. Multiply the length of the loan by the interest rate to calculate the interest rate. Example: You finance $200,000 in 20 years, at 5% per month, and your interest rate is 0.05 x 20.1%. This equals ten bases points.

What are the three most important factors when buying a house?

Location, price and size are the three most important aspects to consider when purchasing any type of home. Location is the location you choose to live. Price is the price you're willing pay for the property. Size refers to the space that you need.

What is a "reverse mortgage"?

Reverse mortgages allow you to borrow money without having to place any equity in your property. It allows you access to your home equity and allow you to live there while drawing down money. There are two types: conventional and government-insured (FHA). You must repay the amount borrowed and pay an origination fee for a conventional reverse loan. FHA insurance covers your repayments.

Statistics

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

External Links

How To

How to buy a mobile house

Mobile homes are homes built on wheels that can be towed behind vehicles. They have been popular since World War II, when they were used by soldiers who had lost their homes during the war. Mobile homes are still popular among those who wish to live in a rural area. These houses come in many sizes and styles. Some houses can be small and others large enough for multiple families. Some are made for pets only!

There are two main types for mobile homes. The first type of mobile home is manufactured in factories. Workers then assemble it piece by piece. This is done before the product is delivered to the customer. You could also make your own mobile home. The first thing you need to do is decide on the size of your mobile home and whether or not it should have plumbing, electricity, or a kitchen stove. Next, ensure you have all necessary materials to build the house. You will need permits to build your home.

You should consider these three points when you are looking for a mobile residence. You may prefer a larger floor space as you won't always have access garage. If you are looking to move into your home quickly, you may want to choose a model that has a greater living area. You should also inspect the trailer. If any part of the frame is damaged, it could cause problems later.

It is important to know your budget before buying a mobile house. It is important to compare prices across different models and manufacturers. It is important to inspect the condition of trailers. There are many financing options available from dealerships, but interest rates can vary depending on who you ask.

Instead of purchasing a mobile home, you can rent one. Renting allows the freedom to test drive one model before you commit. Renting is expensive. Renters usually pay about $300 per month.