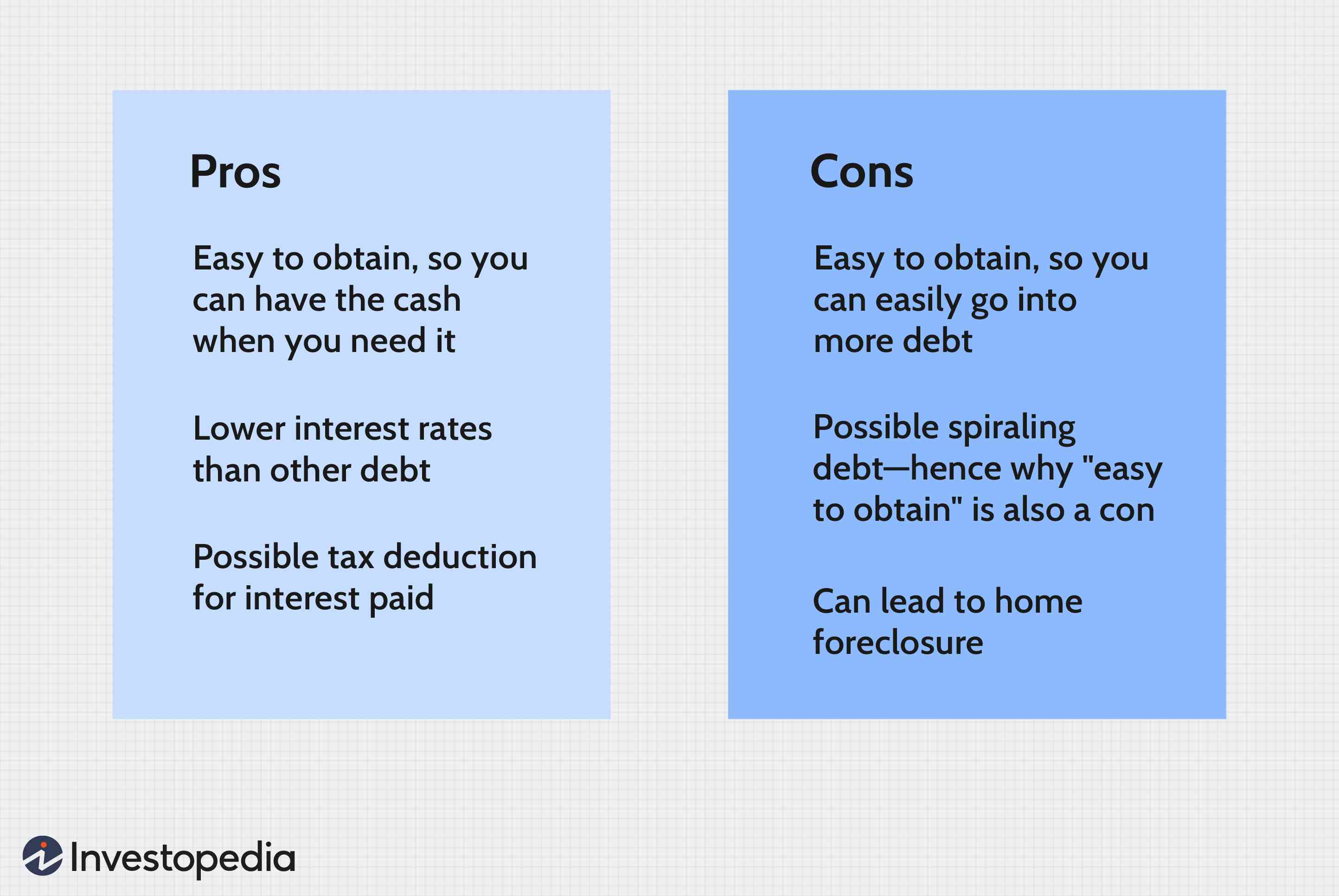

FHA loans can be used for mortgages by first-time buyers. FHA loans have flexible approval requirements. FHA loans require only 3.5% down, and credit scores of 620 or less, as opposed to the 6% required by conventional loans. There is no income verification and no home appraisal. FHA streamline offers another benefit: You can get an FHA mortgage even if your home is already owned. You cannot refinance an existing home into a new loan unless it is being used as an investment property. You cannot refinance the old home with an adjustable-rate mortgage or cash-out mortgage.

Multiple FHA loans are subject to certain limits

A borrower cannot have more than one FHA loan at a time. Borrowers can only apply for one FHA loan at once. This rule is not absolute. Under certain circumstances, it is acceptable for a borrower to obtain two FHA loans.

Federal Housing Administration's (HUD) sets the limits for FHA loans. The number of units and location of the property determine how much money you can borrow. For homes with multiple units, the limits are higher.

Minimum down payment

You must deposit at least 10% of the purchase price to be eligible for an FHA loan. The government or state may offer down payment assistance programs if you do not have enough money. Your down payment can also include a gift from close friends and family. As the FHA can't approve loans that require borrowing to cover the down payment, make sure you give a gift and not a loan.

In addition to the down payment, you must meet credit and income requirements. For an FHA loan to be approved, you will need to provide proof that your assets and identity are correct. You must also have at least a 500 credit score to qualify. You will pay more for interest if you have low credit scores.

To be eligible for an FHA loan, you must meet certain requirements

If you are applying for an FHA loan you must show that you can afford the monthly repayments. You can do this by providing proof of your income, such as pay stubs, bank statements, W-2 income statements, and tax returns. Also, you should have enough financial reserves to pay the down payment and closing costs for a new house.

A loan application should also consider your minimum debt-to–income ratio (DTI). The FHA requires borrowers to maintain a DTI of under 43%. Some lenders may allow applicants with higher DTI ratios. In determining your eligibility for loans, credit scores are also important.

Requirements to qualify for an FHA loan after a waiting period

FHA loans are not easy to get a mortgage for people who have low credit ratings or don't have enough money down. Because this loan is insured by government, the interest rates are typically lower than conventional mortgages. FHA lenders don't charge risk-based mortgage insurance. This means that even borrowers who have poor credit ratings will be approved with a higher chance.

There are some questions you might have about your eligibility for a new loan if your home has been foreclosed. To be eligible for an FHA mortgage, you will need to meet certain criteria. The most important criteria are a lower income of 20% and positive credit reports. You also need to make a down payment of 20%. Also, you should be aware of FHA's rules for extenuating circumstances. This can make it easier to obtain an FHA loan.

Ways to qualify for an FHA loan after a waiting period

There are a number of ways to qualify for an FHA loan after completing a waiting period. One way is to prove that you have paid 12 months of mortgage payments and that your credit has improved since the beginning of your waiting period. An FHA loan is only available to those with a minimum credit score of 580. You may need a higher score to qualify for an FHA loan if you have experienced a foreclosure, or another negative event on your credit.

Lenders will sometimes make exceptions for borrowers who have filed bankruptcy. Bankruptcy can be caused by financial hardship, or an unforeseen event such as a medical emergency. Filing for bankruptcy is a big derogatory mark on a credit report, so many people who file for bankruptcy end up giving up on home ownership. After a bankruptcy, an FHA loan can be obtained if you can show that you have made financial improvements.

FAQ

How much will it cost to replace windows

Replacement windows can cost anywhere from $1,500 to $3,000. The cost of replacing all your windows will vary depending upon the size, style and manufacturer of windows.

What are the advantages of a fixed rate mortgage?

A fixed-rate mortgage locks in your interest rate for the term of the loan. This will ensure that there are no rising interest rates. Fixed-rate loan payments have lower interest rates because they are fixed for a certain term.

What are the drawbacks of a fixed rate mortgage?

Fixed-rate loans are more expensive than adjustable-rate mortgages because they have higher initial costs. Additionally, if you decide not to sell your home by the end of the term you could lose a substantial amount due to the difference between your sale price and the outstanding balance.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

External Links

How To

How to buy a mobile house

Mobile homes are homes built on wheels that can be towed behind vehicles. They were first used by soldiers after they lost their homes during World War II. Today, mobile homes are also used by people who want to live out of town. These houses are available in many sizes. Some houses have small footprints, while others can house multiple families. There are some even made just for pets.

There are two main types of mobile homes. The first type of mobile home is manufactured in factories. Workers then assemble it piece by piece. This process takes place before delivery to the customer. Another option is to build your own mobile home yourself. You'll need to decide what size you want and whether it should include electricity, plumbing, or a kitchen stove. Then, you'll need to ensure that you have all the materials needed to construct the house. To build your new home, you will need permits.

There are three things to keep in mind if you're looking to buy a mobile home. A larger model with more floor space is better for those who don't have garage access. A larger living space is a good option if you plan to move in to your home immediately. Third, make sure to inspect the trailer. You could have problems down the road if you damage any parts of the frame.

Before buying a mobile home, you should know how much you can spend. It is crucial to compare prices between various models and manufacturers. Also, take a look at the condition and age of the trailers. There are many financing options available from dealerships, but interest rates can vary depending on who you ask.

An alternative to buying a mobile residence is renting one. Renting allows you to test drive a particular model without making a commitment. Renting is expensive. The average renter pays around $300 per monthly.