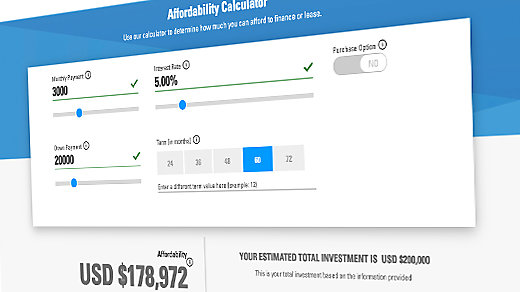

Consider the pros and con's of a HELOC before you apply. HELOCs have no closing costs. However interest charges for funds used for personal expenses aren't tax-deductible. You may end up spending too much on your HELOC and tap out equity. This can lead to high principal and interest costs. The good news is that the interest rates on HELOCs are much lower than those for traditional 30-year fixed rate home equity loans.

Interest charges on funds from HELOCs used to pay off personal costs are no longer tax-deductible

Perhaps you are wondering if your HELOC interest is still tax-deductible. The good news is that you still can up to $750,000 in interest payments on a HELOC. You can't deduct interest paid on funds you use for personal expenses like home renovations. The new tax law has changed how interest payments can now be deducted from personal expenses.

In the past, homeowners could deduct up to $100,000 of interest from their HELOC. The new tax law now limits this deduction to home improvement that increases your home's worth. However, the improvements must be substantial in order to increase the home's overall market value. A substantial renovation is one that significantly increases the home's market value.

The tax code states that interest charges on home equity lines of credit must be paid on collateral. This does not include personal expenses.

There are no closing costs for a HELOC

While no closing costs can be a benefit to a HELOC loan, it is important that you consider all costs before making a decision. You should shop around to find the best closing costs before you make a decision. Closing costs can range from 2% - 5% of the total line credit.

A HELOC is a revolving line of credit that uses the equity in your home as collateral. The funds can be used for a wide range of expenses including home repairs and medical costs. The credit limit is determined by the equity in the property. The "draw period" is generally ten year. Borrowers must repay the loan within ten years. Borrowers might be able to extend the loan if necessary.

HELOC lenders can charge closing costs. However, these fees are typically much less than other costs. Depending on your lender, you may be required to pay an application and origination fee. A notary fee is also possible. These costs will help the lender ensure the loan is legally binding and is not subject to any liens. The lender might also charge for a credit review or an appraisal.

Interest rates are lower than on a 30-year fixed-rate home equity loan

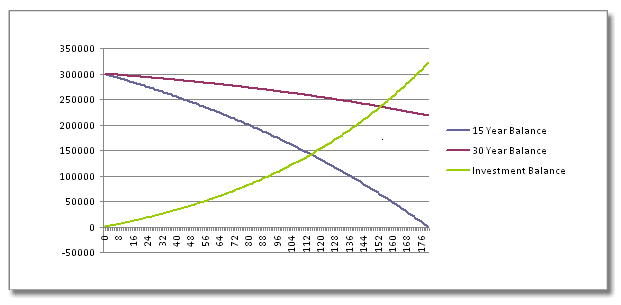

A home equity mortgage is a loan secured by your home's equity. The loan is paid in lump sums, and then repaid over a set period of time with interest. On the other hand, a home equity line of credit (HELOC) functions like a credit card, with the advantage that you only pay interest on the amount borrowed and not the entire balance.

A home equity loans are typically fixed-rate loans with a repayment time of five to thirty years. This means that your interest rate will remain the same regardless of what happens in the economy. Fixed-rate home equity loans typically have lower interest rates than other types of loans. Sometimes, they can even be as low as 3%.

Home equity credit lines allow borrowers access to funds as and when needed. They are the perfect option if you want to make a home improvement project or pay off debt. These lines of credit offer lower interest rates that other loans but require a good credit rating and a low debt to income ratio.

FAQ

What are the top three factors in buying a home?

The three main factors in any home purchase are location, price, size. The location refers to the place you would like to live. Price refers the amount that you are willing and able to pay for the property. Size refers to how much space you need.

Are flood insurance necessary?

Flood Insurance protects from flood-related damage. Flood insurance protects your possessions and your mortgage payments. Learn more about flood insurance here.

How much does it cost to replace windows?

Window replacement costs range from $1,500 to $3,000 per window. The exact size, style, brand, and cost of all windows replacement will vary depending on what you choose.

How much money do I need to save before buying a home?

It all depends on how many years you plan to remain there. Save now if the goal is to stay for at most five years. However, if you're planning on moving within two years, you don’t need to worry.

What's the time frame to get a loan approved?

It all depends on your credit score, income level, and type of loan. It usually takes between 30 and 60 days to get approved for a mortgage.

Statistics

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

External Links

How To

How to Buy a Mobile Home

Mobile homes are homes built on wheels that can be towed behind vehicles. Mobile homes are popular since World War II. They were originally used by soldiers who lost their homes during wartime. People who live far from the city can also use mobile homes. These houses come in many sizes and styles. Some houses can be small and others large enough for multiple families. You can even find some that are just for pets!

There are two main types of mobile homes. The first is made in factories, where workers build them one by one. This happens before the product can be delivered to the customer. You could also make your own mobile home. You'll need to decide what size you want and whether it should include electricity, plumbing, or a kitchen stove. Next, ensure you have all necessary materials to build the house. You will need permits to build your home.

There are three things to keep in mind if you're looking to buy a mobile home. A larger model with more floor space is better for those who don't have garage access. A model with more living space might be a better choice if you intend to move into your new home right away. Third, you'll probably want to check the condition of the trailer itself. If any part of the frame is damaged, it could cause problems later.

You should determine how much money you are willing to spend before you buy a mobile home. It is crucial to compare prices between various models and manufacturers. It is important to inspect the condition of trailers. There are many financing options available from dealerships, but interest rates can vary depending on who you ask.

An alternative to buying a mobile residence is renting one. Renting allows you the opportunity to test drive a model before making a purchase. Renting is not cheap. The average renter pays around $300 per monthly.